Affirm

by Affirm, Inc.

About this app

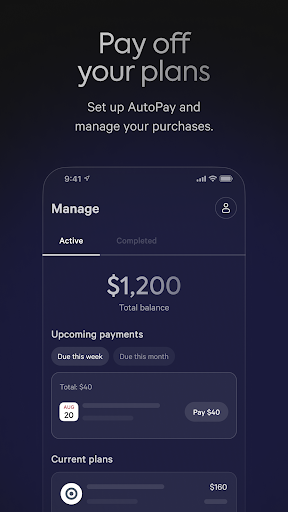

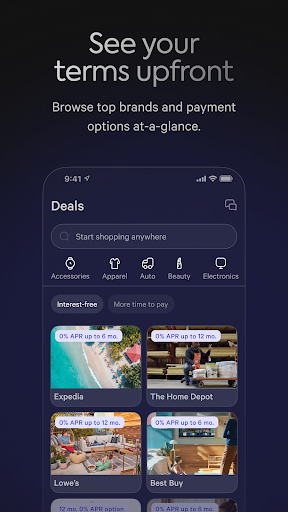

Affirm was founded in 2012 by Max Levchin, one of PayPal's original co-founders, with an explicit mission to build a more honest alternative to credit cards — one where the total cost of borrowing is shown upfront and never obscured by revolving interest. Affirm went public in January 2021 and has established itself as one of the leading buy now pay later platforms in the US, with deep integrations at major retailers including Amazon, Walmart, Peloton, and thousands of smaller merchants. Unlike pay-in-4 competitors such as Afterpay and Klarna's basic tier, Affirm focuses primarily on larger purchases where multi-month financing is more relevant — though it also offers a pay-in-4 product. The Affirm app functions both as a standalone shopping destination and as a financing management tool. Users can browse Affirm's partner merchant directory, generate a virtual card for one-time use at any Mastercard-accepting retailer, and manage all active payment plans from a single dashboard. At checkout with a partner merchant, Affirm performs a soft credit check and presents multiple repayment options: pay in 4 (biweekly, often 0%), or monthly plans from 3 to 36 months at stated APRs that range from 0% on promotional offers to 36% depending on creditworthiness and merchant. The critical differentiator is the upfront total: before you confirm, you see exactly how much you will pay in interest, and that number never changes — no late fees, no compound interest surprises. Affirm is best suited for deliberate, planned purchases above $100 where spreading cost over time is a genuine financial planning tool rather than an impulse enabler. It is used most effectively by consumers who would otherwise put the purchase on a high-APR credit card, where Affirm's locked rate can be cheaper. The risk is the same as any credit product: taking on installment obligations across multiple purchases simultaneously can obscure total debt load. Affirm is more transparent than traditional credit cards, but transparency alone does not eliminate the underlying financial risk of spending money you do not yet have.

Features

- →Total Cost Transparency — Shows exact total interest and payment amounts before confirmation — the figure never changes due to late fees or compounding.

- →Virtual Card — Generate a single-use Affirm virtual Mastercard to use BNPL financing at any retailer that accepts Mastercard, even without a direct Affirm integration.

- →Flexible Loan Terms — Choose repayment schedules from 4 biweekly payments to 36 monthly installments depending on merchant and purchase size.

- →Payment Dashboard — View all active Affirm loans, upcoming payment dates, and remaining balances from a single centralized management screen.

Final take

Affirm stands out in the BNPL category for its genuine commitment to fee transparency and its focus on larger, considered purchases rather than impulse fashion buys. If you are going to finance a purchase, Affirm's no-hidden-fees model is the right way to do it. Just be honest with yourself about whether the purchase is necessary — financing clarity doesn't replace financial discipline.

Pros

- ✓Fully transparent about total loan cost upfront — the final amount shown at checkout is exactly what you pay

- ✓Flexible repayment terms from 3 to 36 months accommodate both small and large purchases

- ✓Soft credit check for pre-qualification does not impact your credit score

Cons

- ✗Interest rates (APR 0-36%) can be high for borrowers with lower credit scores — always calculate total cost before committing

- ✗Using BNPL for discretionary spending can accelerate debt accumulation for users already managing tight budgets

- ✗Not all retailers offer 0% APR promotional terms — many everyday purchases carry interest charges